When lawmakers propose solutions to complex economic problems, the first requirement should be a clear understanding of how those problems actually work.

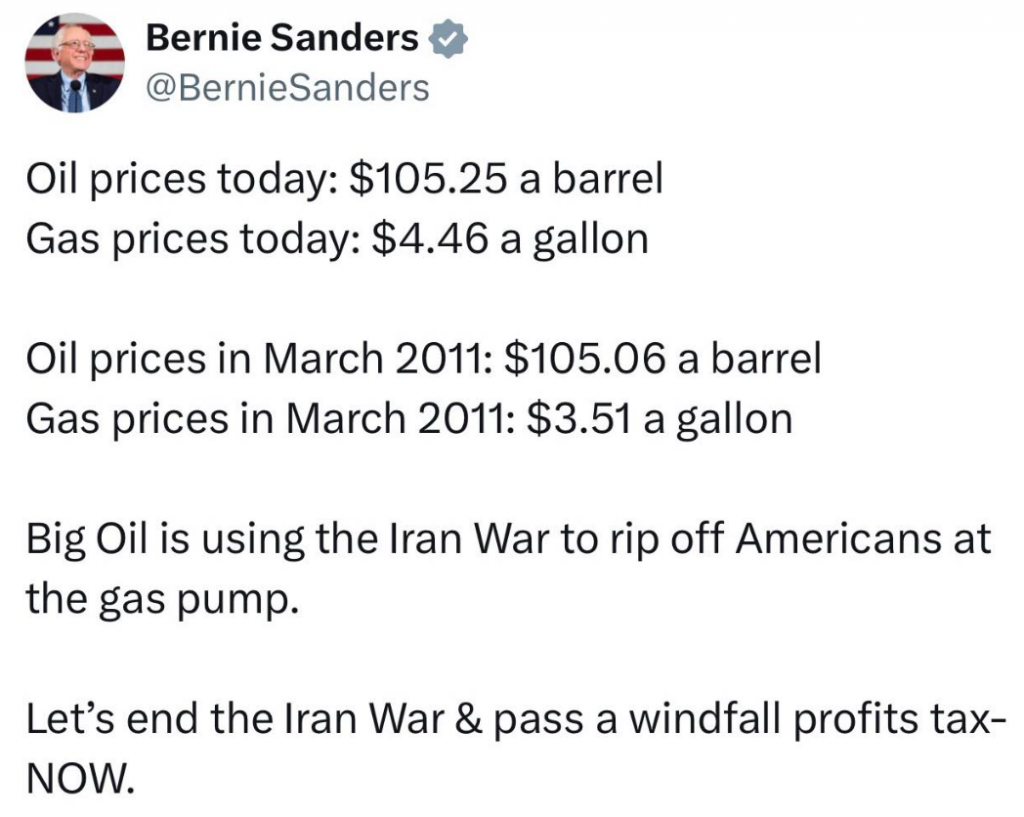

A recent Facebook post by Bernie Sanders comparing today’s oil and gasoline prices to those in 2011 suggests that oil companies are “ripping off” consumers. The logic is straightforward: if oil prices are roughly the same, gasoline prices should be as well. If they aren’t, someone must be taking advantage.

It’s an intuitive argument, but it misses important elements of the story.

Although gasoline prices have a high degree of correlation with crude oil prices, there are many reasons those prices can diverge. Gasoline is a manufactured product that sits at the end of a long, complex, and often strained supply chain. Focusing only on the price of a barrel of oil ignores the physical realities that determine what consumers ultimately pay at the pump.

From Crude to Gasoline: A System Under Strain

The price of crude oil is only the starting point. Between the wellhead and the gas station lies a network of refineries, pipelines, storage terminals, and transportation systems.

When that system is operating smoothly, the relationship between oil and gasoline prices is relatively stable. When it isn’t, the two can diverge significantly.

That is exactly what we are seeing today.

The Refining Constraint Most People Miss

One of the biggest differences between 2011 and today is refining capacity.

Over the past decade, the U.S. and parts of Europe have lost meaningful refining capacity due to closures, conversions to renewable fuels, and underinvestment. At the same time, demand has rebounded strongly following the COVID-19 pandemic.

The result is a system that is running with very little slack. Refinery utilization rates are often in the mid-90% range. At those levels, even minor disruptions can have an outsized impact.

This is where the concept of the “crack spread” comes into play. It reflects the margin refiners earn by turning crude oil into gasoline and diesel. When capacity is tight, those margins expand. That can push gasoline prices higher even if crude oil prices remain relatively stable.

In other words, you can have plenty of oil available and still face high fuel prices because the bottleneck is not supply of crude, but the ability to process it.

War Doesn’t Just Raise Prices. It Disrupts Systems

The current geopolitical environment adds another layer of complexity.

Conflicts in key regions, including tensions involving the Strait of Hormuz, do not simply raise oil prices. They disrupt logistics. Shipping routes change. Insurance costs rise. Delivery times increase. Supply chains become less efficient.

Refineries are also highly specialized. They are designed to process specific grades of crude oil. When geopolitical disruptions force a shift in sourcing, refiners may have to run less optimal feedstocks, which can reduce the yield of gasoline per barrel. This is also what happened following Russia’s invasion in Ukraine, which results in skyrocketed diesel and gasoline prices.

These are mechanical, physical constraints. They act like a hidden tax on the system, increasing the cost of producing and delivering fuel even if the headline price of crude oil appears unchanged.

This Isn’t New. It’s Just Misunderstood

The divergence between oil and gasoline prices is not a new phenomenon.

After Hurricane Katrina in 2005, for example, crude oil prices softened because refineries were offline and couldn’t process available supply. At the same time, gasoline prices surged due to shortages of finished fuel.

The lesson is simple: the energy system behaves like a chain. If one link breaks or tightens, the entire system adjusts. Prices reflect those constraints.

What we are seeing today is a similar dynamic, driven not by a hurricane but by geopolitical disruption and structural changes in refining capacity.

Profits Are the Result, Not the Cause

It is true that energy companies are reporting strong profits. But those profits are largely a consequence of high prices, not the underlying cause of them.

When supply is constrained and demand remains strong, prices rise. When prices rise, profits follow.

That distinction is important. If high prices were simply the result of companies choosing to charge more, the solution would be straightforward. But when prices are driven by physical constraints, logistical friction, and global market dynamics, the problem is far more complex.

The Risk of Misdiagnosing the Problem

Policies like windfall profits taxes are often proposed as a response to high energy prices. But if the diagnosis is wrong, the prescription can make the situation worse.

Discouraging investment in refining and midstream infrastructure does not lower prices. It tightens capacity further, increasing the likelihood of future price spikes.

If the goal is to bring down fuel costs, the focus should be on improving system capacity, reducing bottlenecks, and stabilizing supply chains.

The Bottom Line

Comparing oil prices across time periods without accounting for the broader system leads to misleading conclusions.

Gasoline prices are shaped by far more than the cost of crude. Refining capacity, logistics, geopolitics, and infrastructure constraints all play critical roles.

If policymakers want to address high fuel prices effectively, they must start with a clear understanding of those realities.

Because in energy markets, as in economics more broadly, getting the diagnosis right is the first step toward getting the solution right.

Follow Robert Rapier on LinkedIn or Facebook