Whenever I try to get a feel for the direction of natural gas prices, the Energy Information Administration’s (EIA) Weekly Natural Gas Storage Report is the first place I stop.

This report provides an update on the levels of natural gas in storage facilities across the United States. The report includes data on working gas in underground storage, with details on net changes, implied flows, and comparisons to historical data. It’s released every Thursday and covers data up to the previous Friday. The report is a key indicator of the natural gas supply and demand balance and can impact prices in the natural gas market.

Seasonality also plays a big factor in natural gas prices. Because natural gas demand spikes in the winter, producers use underground pressurized storage that builds inventories from spring until mid-fall. During the winter heating season, this storage is depleted.

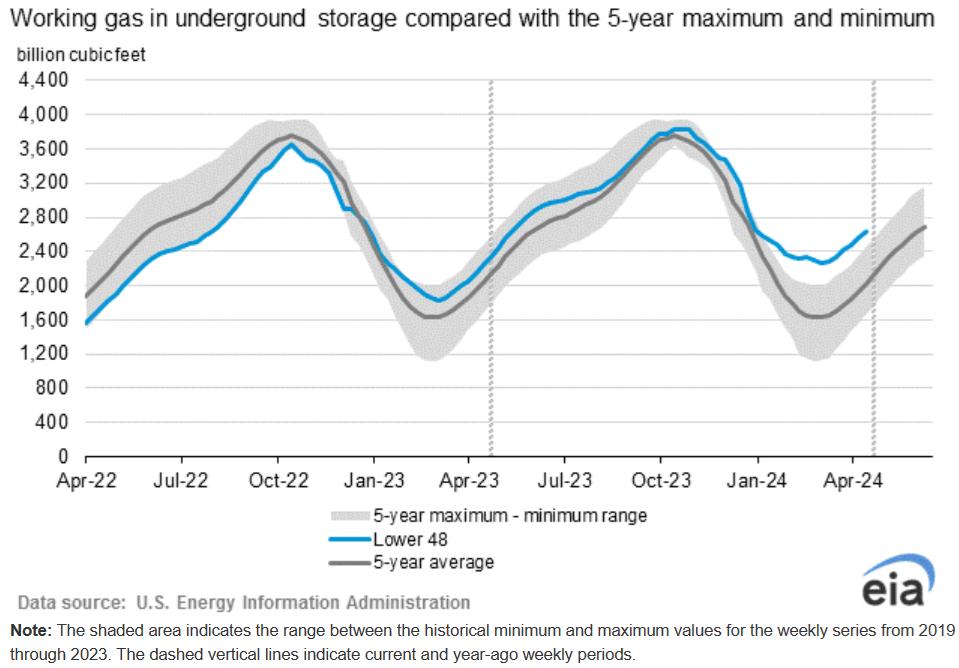

Note in the graphic above that the U.S. exited the winter season with inventories above the 5-year maximum range. Natural gas inventories are 19% higher than they were a year ago, and 31% above the 5-year average.

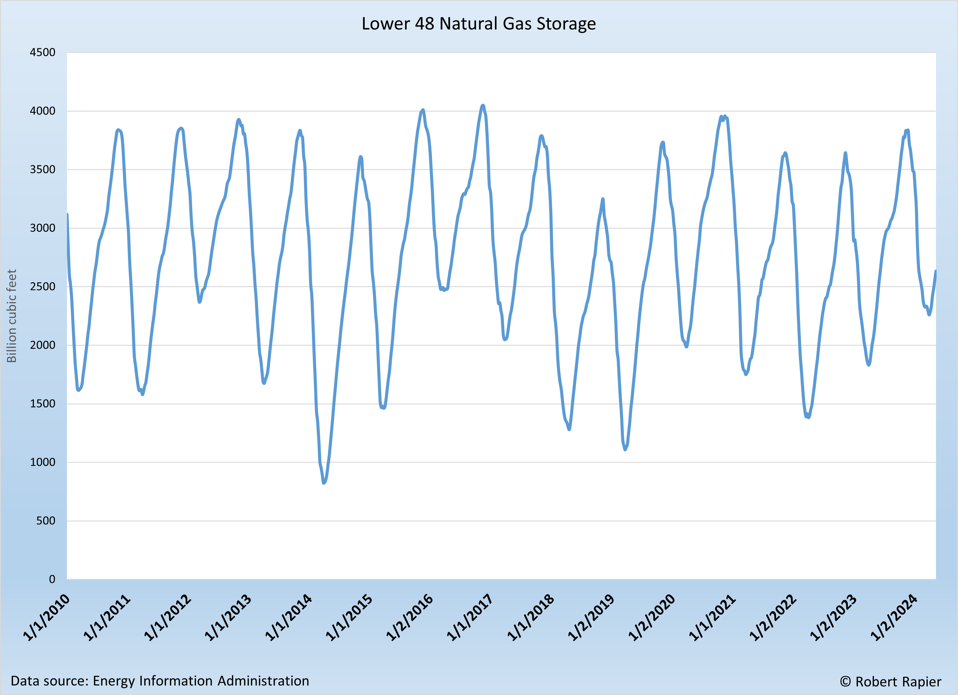

Inventories are high due to a combination of U.S. production outpacing demand growth, but also due to soft demand due to more warmer winters in recent years. This can be seen in the following graphic.

In the case of a mild winter as in 2012, inventories were not significantly depleted before they began to rebuild. The winter of 2011-2012 failed to pull gas inventories below 2 trillion cubic feet (Tcf) for the first time in over 20 years. Inventories in 2012 bottomed out in early March above 2 Tcf, which was also two to four weeks earlier than is typical. As a result, natural gas spot prices collapsed to under $2 per million Btu (MMBtu), and they didn’t recover back to the $4/MMBtu level for a full year.

The situation was quite different in the winter of 2013-14 when natural gas inventories were substantially depleted. That inventory situation resulted in natural gas price spikes which exceeded $8/MMBtu at one point, and elevated natural gas prices for the next year.

The current situation is reminiscent of those mild winters of 2012 and 2016, both of which ushered in an extended period of depressed natural gas prices. Unsurprisingly, given the current inventory situation, natural gas prices recently fell below $2/MMBtu. If history is any guide, prices are likely to remain depressed relative to historical averages until we once again have a colder winter season.

However, one significant difference between the situations in 2012 and 2016 and now is the growing exports of U.S. liquefied natural gas (LNG). Those exports have the potential to consume the excess supply and bring the supply/demand back in balance much sooner than happened in previous years.

Follow Robert Rapier on Twitter, LinkedIn, or Facebook